Considering a Management Buyout (MBO)?

– Part 4 of a 5 part series on MBOs

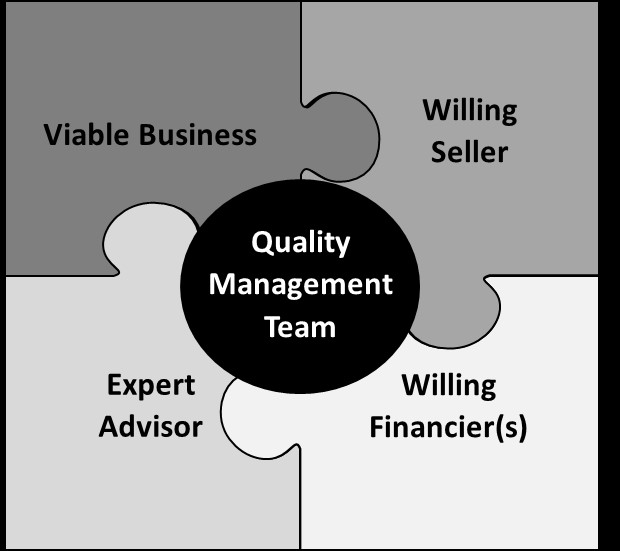

Critical Success Factors

Management Team

Corporate financiers will often say that the three most important ingredients for a successful MBO are “management, management, management” meaning that the quality of the management team is the most important element of a successful MBO. Financiers need to be convinced that the team has the all-round strength to manage the business independently. A high level of commitment to the MBO and to its subsequent successful growth is also essential. Entrepreneurship is key here but the management team must also have a clear strategy for building the business.

In general, the management team will include up to three or four managers. Other managers and staff may also be given the opportunity of investing, although this can be done through stock options. The management team needs to be complete, competent and committed. A complete team will normally consist of the following (although will vary from industry to industry):

- CEO/President/Managing Director – a leader with experience, ambition and vision,

000who has held full profit responsibility in the business or elsewhere. - CFO/Controller – capable of maintaining the financial discipline and control required

000to manage the business finances and to ensure that the deal financing is repaid. - COO/Operations Director – a technically proficient person who understands the

000technology and processes of the business. - VP/Director of Sales – an experienced customer focused sales person with a good

000commercial understanding.

The team needs to be balanced and its individuals need to work well together. On occasion if there is a good but partial team, a manager can be added to complete it. Competence will be assessed by reviewing the track record of the business, the CVs of the individuals concerned and an assessment of their credibility in delivering the plan for the business. Commitment is usually ensured by requiring all of the MBO team to personally invest in the deal. The importance of the management team cannot be over emphasized – financiers are backing the team to deliver. Management will also need to convince its backers that it has a sound growth strategy and that they are capable of implementing it. It is also vital for the smooth running of the deal to appoint an expert adviser at the outset who will project manage the MBO on a day to day basis, co-ordinate the various parties involved and drive the timetable through to a successful conclusion.

How much money will we need to invest personally?

Each member of the management team is expected to invest personally. The amounts involved are intended to signify commitment from the individuals concerned but will be small relative to the total size of the financing required. The team leader/CEO will usually invest more than other key team members. A “rule of thumb” is for the CEO to invest around one times their annual salary but it will depend upon personal circumstances. It is quite common for members of the management team to borrow money from a bank in a personal capacity to finance their investment (your adviser can guide you on this aspect). Should the management team already have some stock or options in the target business, the financiers will expect them to reinvest their capital gains. They want management to be “buyers” not “sellers”.

Viable Business

The business must be capable of operating independently as a commercially viable entity. This is especially important when it concerns an MBO of a division of a larger company. Here you will need to ensure the company must not be overly dependent on inter-company sales. It must have sufficient critical mass on its own. It must have access to the intellectual property – patents, trademarks, licenses. There must be no dependence on group/shared services such as distribution, sales, and finance. The management team will need a robustly constructed business plan that details a demonstrable growth strategy, one that has a strong competitive position, preferably in a growing sector.

Willing Seller

Clearly without a willing seller who is prepared to sell at a realistic price, there can be no deal. Management needs to understand the seller’s motivations. What is the seller’s rationale for selling the business? Why does the seller want out? What are his motivations? Many sellers may not consider an MBO until it is suggested to them. At the first opportunity, it is up to the management team to take charge of the situation when it appears as if its company might come up for sale or, in the case of a private company, where factors such as the owner’s age or health may be becoming a factor. Equally, in suggesting the idea of an MBO to the shareholders, the management team has to point out the advantages over an external sale. Initiating MBO discussions can be delicate and advice is important.

When should management approach the seller?

The seller will need to be approached early on in the process. It will depend on individual circumstances as to who should approach the seller – either the management team or the adviser. Before making a formal approach to the seller it is sensible for your adviser to undertake an initial feasibility study to confirm that any proposed deal will be viable and fundable. Dealings with the seller need to be handled carefully as the team will be employed by the business during the MBO process and likely thereafter if a deal is not closed. Sensitivity and discretion are paramount. Until seller approval has been received to progress the MBO opportunity, care should be taken to observe your fiduciary duties as managers/directors. The timing and nature of the approach is a critical area and one in which your adviser will guide you.

Willing Financier(s)

In order to be able to buy the company, the management team needs the financial backing of private equity firms and banks to provide equity and debt capital. Private equity firms look for stable and growing businesses with a strong management team. They like to invest in companies with a potentially leading and defendable market position and growth prospects. In order for the private firms to make a return on their investment and that of the management team, it is important that there is a suitable exit opportunity in the future.

Why are exit opportunities so important in an MBO?

Before your financiers invest they will want to assess the opportunities for selling. This may seem somewhat premature but remember the private equity firm (and management team) realize their gains predominantly on exit so, how, when, and to whom they will exit is key to their investment realization. Private equity firms need to be able to realize the value of their equity at a significant capital profit often over a three to six year horizon. They will achieve this in several ways:

- Buyer: A sale of the company to an external buyer

- Private equity firm: Sale of the company to another private equity firm

- Management: may occasionally be able to buy out the shares of the private

000equity firm through a secondary fund raising - Stock Exchange: A flotation of the business on a stock exchange

The most likely exit route will be a sale of the business to an external buyer and the private equity firm will want to be satisfied before investing that a pool of potential buyers exists. The business must be attractive to future buyers and make a lucrative proposition to them.